The Federal Reserve’s FraudClassifier divides fraud into two categories: authorized fraud and its unauthorized counterpart.

Authorized fraud occurs when a legitimate party initiates a payment only to have a bad actor intervene and hijack the funds. Unauthorized fraud, on the other hand, happens when bad actors initiate or redirect a payment through an account takeover or by stealing account-holder credentials.

Although the first of these — authorized fraud — accounts for only 37% of the losses financial institutions (FIs) must absorb, it’s the form of fraud that will most likely undermine customer satisfaction and retention.

The PYMNTS Intelligence report “Leveraging AI and ML to Thwart Scammers” found that fraud incidents continue to plague FIs and their customers, despite ongoing efforts to educate consumers on steps they can take to protect themselves.

The size of the institution does not shield it from fraud. In most cases, the bigger the FI, the more likely that incidents of authorized fraud climb, peaking at 46% for those FIs with more than $100 billion in assets under management (AUM). The smallest FI respondents PYMNTS studied — those with between $1 billion and $5 billion in AUM — are the exception to this rule. They endure the second-highest authorized fraud rate of 43%.

The share of total dollars lost also increases with FI size, reaching a high of 44% for FIs with more than $100 billion in assets. However, it’s often the FI’s customers that absorb the losses because they authorized the transactions, and this potentially explains why authorized fraud is so destructive to customer relationships.

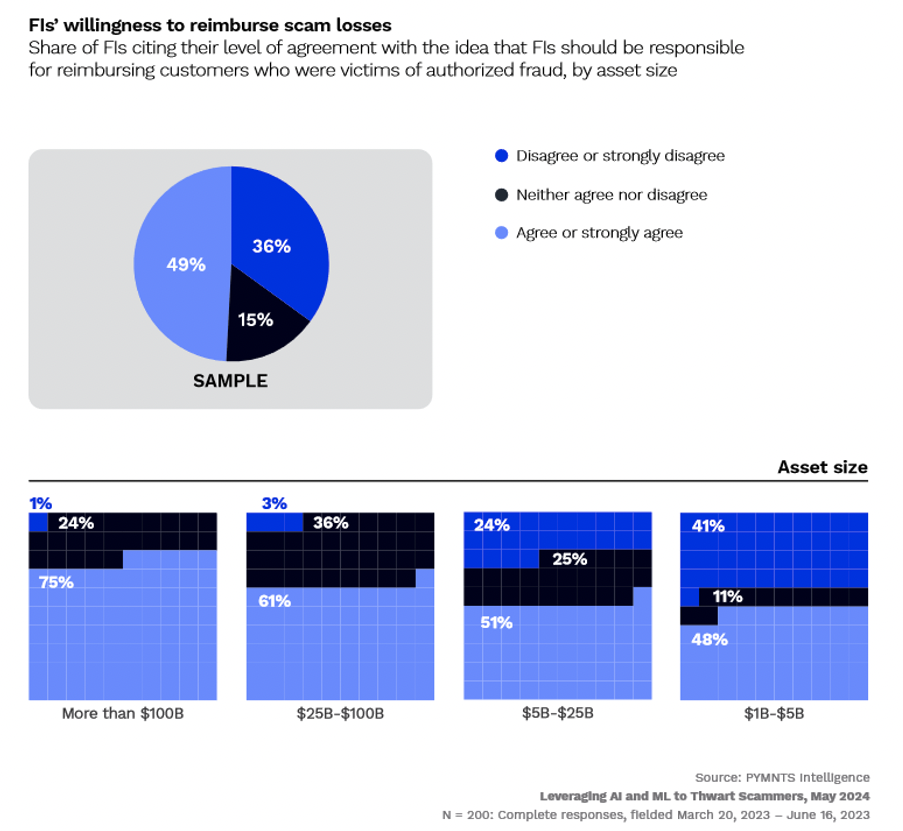

To offset the damage, 49% of all FIs agree that they should be responsible for reimbursing customers victimized by authorized fraud.

To offset the damage, 49% of all FIs agree that they should be responsible for reimbursing customers victimized by authorized fraud.

Even though larger FIs see a higher portion of scams, they are also the ones most likely to agree they should reimburse their customers for losses triggered by authorized fraud, at 75%.

Sixty-one percent of the next tier of FIs ($25 billion to $100 billion in AUM) said they should cover the fraud losses, while 51% of FIs with $5 billion to $25 billion in AUM said they should cover the costs. Meanwhile, refunding customers may be too harmful to the bottom lines of smaller FIs, which might be why a lower share, 48%, said they are willing to do so, meaning they more knowingly run the risk of losing customers rather than forfeiting funds.

FIs can educate their customers about the latest fraud schemes, particularly authorized fraud, but despite their best efforts, they will likely find themselves choosing between covering the costs of fraud reimbursement or living with the costs of lost customers and reputational damage.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More